Cusp of pain, We Are As Gods

Near-term economic negatives. Bring back the woolly mammoth? Me on ESG. Jamie Dimon (JP Morgan CEO) on ESG. Grenfell.

This week’s mostly about the economic pain coming (although spring follows winter), Stewart Brand’s techno-optimism, and links.

I have the transcript of my ESG and investing chat including taking you from Malthus through Milton Friedman to stakeholder capitalism today. Link here, also to podcast.

Near-term economic negatives

My friend, Jane Soliman, curated Latin American women artists’ exhibition (London)

My friend, Naomi Kerbel, podcast; Shop pre-loved

Also, my friend, Dana Perkins podcast on EU Energy focus

Oral history, video histories, documentaries: advice, ideas?

London Climate week coming up 25 Jun - 3 July

Jamie Dimon (JP Morgan CEO) on ESG

Me on ESG

We Are As Gods, Stuart Brand documentary

Grenfell, docu-drama, verbatim play

Links: Changing Fed expectations, green capitalism, homeless in Houston, Stuart hall; Web 3.0 broken contracts; podcasts.

As regular readers know, on average I am a long-term optimist. I believe optimism is the most helpful outlook and mirrors the generational trends we’ve seen in the last 150 years on human progress such as life expectancy and healthcare. I’m also syncretic and reasonably pragmatic.

Right now, I judge, we stand (70% chance) on a short-term negative cusp which will be / and is already, painful for many people (though maybe not for the readers of this letter) and could well last into 2023. With unfortunate events it could drag into 2024. Let me briefly outline some of the reasons, and perhaps some things to think about if/when we do head into recession (personal views yadda yadda).

The intersectional reasons are:

Geopolitics: Russia <--> Ukraine

→ Inflation in energy and food, increased geopolitical risks (also including China; but a whole new cold war axis building eg Russia-China-India); also other possible shortages, eg Neon

→ “Cost of living crisis” → Many dropping below poverty line, and those below struggling. Middle class being squeezed.

China Supply Chain issues (stemming from COVID and lockdowns) with global impacts (albeit somewhat temporary, there is re-localisation of supply chain in the long-term)

COVID cost on health, and more economic head winds (long COVID, productivity, more cancellation; more strain on overall health services)

Rising interest rates, and high forward looking costs of borrowing (to combat inflation). The long term US mortgage rates risen to levels last seen pre-2010 and likely rising more.

Negative “Real wages”; so wages minus impacts of inflation, so lower income power from consumers

No/limited access to capital for start-up companies (tech, biotech, climate tech; though strategic partners eg larger companies still have cash), small businesses; Tech people lay offs, so job losses in certain sectors,

Many weakened industries due to COVID impacts (eg theatre, restaurants, events etc. there is some rebound, but still facing headwinds eg travel is harder)

Crypto crash and c. $2,000 billion crypto wealth destruction over the last year; similar for losses in US markets, and same again in non-US markets. There is potentially a negative “wealth effect”

There is a partial offset from hybrid remote working (for some people but often not front line), and some areas of innovation (eg biotech, software) are still progressing. Longer-term many elements of progress still in place.

Let’s examine these in turn:

→ Inflation in energy and food, increased geopolitical risks (also including China; but a whole new cold war axis building eg Russia-China-India).

The root cause of inflation is not only Russia-Ukraine, China, although it’s a factor (supply constraints). The root cause likely seems also to be in part the money spent by governments over the pandemic (demand side). The causes are also a little different in US and EU (see Jason Furman, others on this). Still inflation is now here, in part temporary, but in part structural and in part both supply and demand; and all kinds of negative impacts are following. (This is also where there is a lot of doubt, because if the inflation is almost all temporary supply chain issues then some of this might go away; hence as ever nothing is certain; many smart economists are arguing over this right now).

Russia-Ukraine is causing a crystalisation of a new chapter of geopolitical conflict. It seems clear to me that the vast majority of people in Europe and the US are blind to what is happening. Russia has significant support from China and India, and moderate support from many countries.

(as of April 2022)

Putin has plenty of internal support.

This conflict and the associated economic costs (via deglobalisation, food, energy, sanctions) are likely to drag on for some time, and even when/if they moderate will unlikely disappear to zero. The geopolitics is not only increasing risk, and uncertainty (and thus bad for business and people); but is having direct economic action impacts via trade (and food, energy prices)

Prediction markets imply c.35% change of cease fire before year end, and this has been in decline this year.

The geopolitical risks are leading to deglobalisation and a re-localisation of supply chains to a certain degree. This gives more resiliency, but at higher cost, and higher costs for consumers (lthough perhaps better for the environment).

Inflation and economic costs are in turn hitting the poor, and even the middle class, in almost every nation. The “cost of living crisis”. People are eating into their savings where they have them, or relying on charity where not. This is why we can see the crisis coming.

The poor spend much more on food and energy and there is some evidence that inflation is also hitting them harder (as certain cheaper foods increase more, paying energy by the week or prepayment is more expensive than direct debit in advance etc.); lack of access to the internet means less acess to better prices).

On top of that, COVID is a drag and will remain a permanent drag. The flu costs the US about $90bn a year. The flu costs the UK about GBP30bn a year. COVID will cost more, and this is a permanent negative cost (long term there may be an offset from mRNA technology development, but not in the short term). The impacts of long COVID could be in the order of $2,000 bn* (I view this as a high estimate, but Harvard economist David Cutler has made it1), in any event we have limited near term growth prospects to overcome this structural head wind. This will put a permanent increase strain on health systems eg UK. Certain industries eg events, may also see a drag for some time.

Rising interest rates, and high forward looking costs of borrowing (to combat inflation). The long term US mortgage rates risen to levels last seen pre-2010 and likely rising more.

The challenge of inflation is leading central banks to raise interest rates (and “tighten” in quantitative tightening or QT, the reversing of QE, or quantitative easing, a process started in the GFC of c. 2008). This is leading - amongst other factors - to a higher cost of money, leading to lower valuations for all equities, especially equities based on future value (tech, innovation); rising mortgage rates, higher cost of borrowing for all loans.

The US cost of home borrowing is now above pre-2010 levels and likely to keep rising. 6%+ on the typical mortgage.

Some observers will argue that at certain level of decline, the Fed / central banks will stop QT/rising rates (and in reverse) even before inflation goes back down to 2%: but no one knows what this level is on stock indices. Negative 10%, 20%, 30%, 50%; what level of GDP / recession? And no one knows the possible overshoot on the way down.

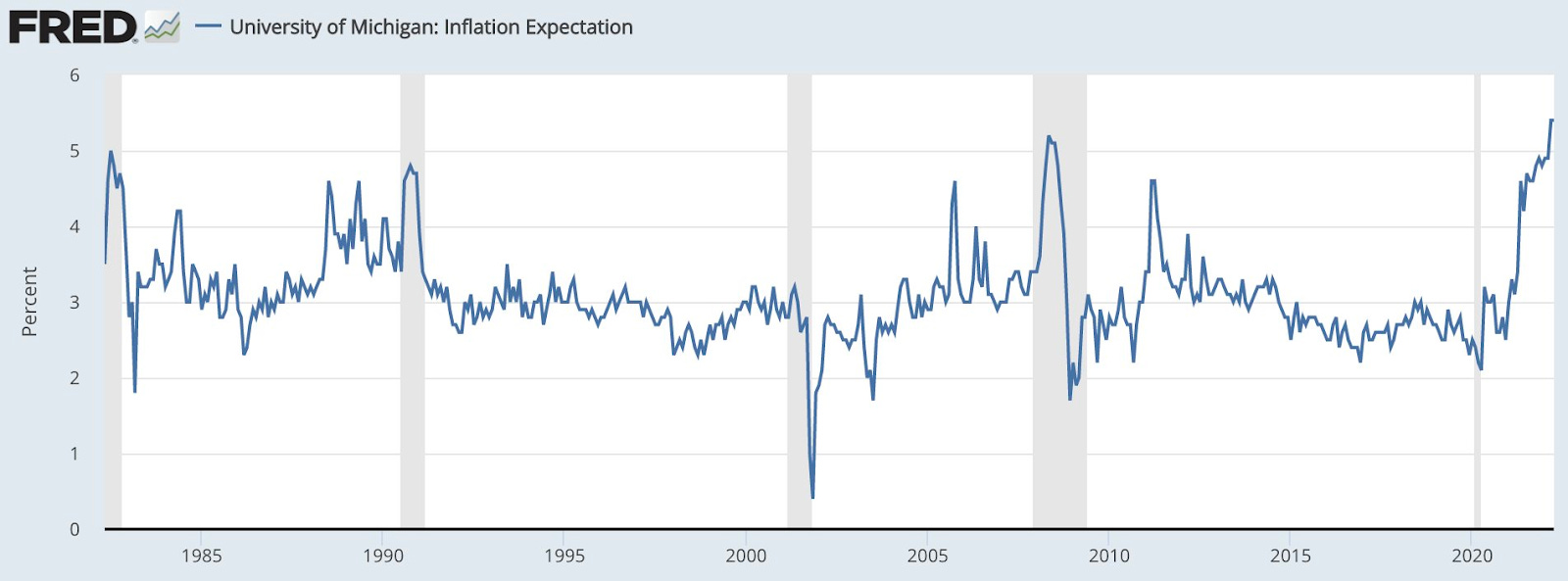

Surveys of consumer expectations are rising. The long running Uni of Michigan (US), inflation expectations (so survey data of real people) has hit 5.4% a number last seen pre 1982.

The FED does not want to see this anchored at these levels. There is a conisderable theory that behavioural anchoring mkes a difference to actual inflation via mechanisms such as wage bargaining (and UK rail unions certainly seem to be influenced by this)..

Access to financing has dried up for most companies needing/wanting capital. This is the winter for start-ups. VCs do still have some capital, as do large companies, but no one is deploying it until there is more clarity on the economic cycle, and the valuations that will be deployed at will be significantly lower than 2019-2021.

An unknown number of people / entities have seen their crypto wealth destroyed, and it seems unlikely that it will return in 2 years, and possibly for some never. There have been significant insolvencies and contract breaches in web 3.0. The 2017 Bitcoin high (>19,000) was not reached again until end of 2020. Given the economic backdrop, at least 3 years - so 2025 (if ever) in reaching the 2021 highs (>60,000, range 30,000 - 60,000) seems very plausible scenario. (ofc, there are Crypto HODLs on the other side of this, but most of them have not seen crypto in a recession). No science here, so I suppose anything is possible. Many smart people see zero real world use case for crypto so perhaps it goes down close to zero.

There has also been some equities wealth destruction, but pension funds that had managed to reach fully funded status in 2020-2021 have likely slipped back into under funded status again unless they managed to liability match.

The financial world is not the physical world, but financials intersect and interconnect in the most profound ways. All the current happenings point to significant and increasing stress now and for several months, likely into 2023 especially for poor people.

The near term policy and business response is unclear. Over the medium term, spring follows winter, but it seems likely that winter is coming; and for many is already here.

For many of you reading this letter, you will be OK but it might be time to think on a few things.

Be mentally prepared. Mental resilience can be a learned and practise skill. It may be that you will be more mentally stressed in the coming months. This cycle will turn up again, but you have to have the mindset which can be there for the spring after winter.

Most ordinary investors have limited options when mainstream assets (equities and bonds) fall (and fall togther). But you can still invest in yourself by learning useful skills, “building things”, investing in your social networks, ideas etc. If you have a certain level of wealth and know me, we could chat some other things one can do. You can always have dry powder to invest even in winter. And do note over a longer time, eg a 7 year cycle, you will like be back in the black.

Be there for friends who might struggle. Supporting friends during the recission is going to feel different to the pandemic, with high inflation and possible job losses causing even more unequal impact. Still, mostly middle classes will be fine-ish I think even if the mood will be sour.

On a happier note…Oral history, video histories, documentaries: advice, ideas?

On the arts side, we and Transport Sparks might be embarking on a form of video or oral history documentary. Anyone with any ideas or experience here, happy to hear advice. This is young people on the autistic spectrum and their love of transport-related things. Message me.

I thought I’d highlight the women friends who are doing great things.

Pre-loved and second hand. My friend Naomi Kerbel has a podcast and her latest podcast episode is about the trend for pre-loved on the back of the eBay/ Love Island partnership, including tips on how to shop second hand. As an aside, I’ve an interest in a second hand search app, Ask Loma, https://lomasearch.com/ (feedback to Joseph Undaloc) and Used and Loved are looking to raise https://usedandloved.com/crowdfunding (link with Jessica Potter)

My friend, Jane Soliman, curating a Latin American women artists exhibition (London). Opposing Fictions: Women Provoking Fact & Fabrication

Amalgama Art, a London-based cultural platform dedicated to promoting women artists from Latin America, is launching its 2022 Group Exhibition on Tuesday 21 June. Opposing Fictions: women provoking fact and fabrication, an exhibition of Latin American artists whose work challenges our understanding of the imaginary in an age of factual uncertainty. Check out: (artamalgama.com) Venue: Koppel X, Piccadilly Circus (next to Boots), London W1B 5RA. Private View: Tuesday 21 June 2022, 6-8pm. If it might be your thing…. RSVP: https://www.artamalgama.com/event-info/PV-OpposingFictions

Also, my friend, Dana Perkins has a podcast all thing energy related, most recently with an EU Energy focus. Check it out here.

In the world of ESG… Jamie Dimon said this:

“I am a red-blooded free market capitalist and I'm not woke. People are mistaking the shareholder – stakeholder capitalism thing for being woke. All we said for stakeholder capitalism is when you say to me, when you say to Americans ... there are 325 million Americans, and when you say shareholder value and fiduciary responsibility, they hear short-term profit taking at the expense of employees or customers. And fiduciary, they hear, high paid lawyers protecting CEOs. All we're saying is when we wake up in the morning, what we care about is serving customers, earning their respect, earning their repeat business. And we do that through employees. And that's what we do. …

… when we do things like climate, we're quite serious about climate. I don't think America is getting climate right. I think the chances of getting it right, is virtually nil. I don't think we remotely understand the complexity of this, and we can't turn on electricity from hydroelectric power as much less. ... We're not getting it right because it's uncoordinated. We're confused between hugging trees and yelling at the lending. ... we need real leadership in this area and we're not getting it.

…if you're an employee of ours and whether you're black or white, Jewish, or Muslim, Indian, Asian, disabled, LGBT+, we want you to be treated with respect in our company. We want to give you opportunity, that's not woke. ..we want.. that you can contribute to the company to the best of your ability. Any senator says that's woke, they're not thinking clearly. I want to win in the marketplace. I want the best employees. I want happy employees.

…[Private Equity] don't have to deal with Glass Lewis and ISS, which shame on you if any of you – if that's how you vote, shame on you.

…. So the lead director goes up there. They talk to a 27-year-old compliance officer who writes a memo, and then votes Glass Lewis.

I think if we send up a director of ours who's a decision maker, they should sit with someone from your side who is a decision maker and you should be able to say to that person on the spot, you've got my vote, or you don't. As opposed to, we have to wait until the proxy day. And I just think we're just slowly destroying corporate America for all the wrong reasons. And if you don't fix it, folks, you better go private too, because you are not going to be able to – enough public companies. I don't think it's good for America, because I think our active transparent markets are great. They have been one of the engines – with all the flaws we've had, they've been one of the engines here. So I'm begging you, I'm begging you don't allow this to happen with no aforethought. Figure out what it's going to look like in 10 years and see if that's acceptable, because in my view, it's not.”

Whereas I say…

Matt Orsagh talks with me. We discuss ESG integration, ESG education, demographics, Economist Thomas Malthus, and the future of capitalism. We also talk about current and impending regulation and policy around ESG disclosure as well as the intersection of art and ESG. One section:

You are someone in 1650, do you think we would ever not have slaves? I'm guessing 99% of people would say, "You'd be crazy. We've had slaves for 4,000 years. Our whole economy would disappear. Why would that be possible?" Yet it was. So fast forward to the 1950s. You had a lot of movements, from faith based and other investors thinking about a kind of ethical or value based judgment about how they would want to invest. They just wanted their investments to reflect their mission and values.

Then you fast forward kind of into the 1980s, 1990s where you had thinkers like Milton Friedman come along thinking about markets and capitalism in that respect. And then 1990s, you started thinking about triple bottom line, a lot of talk about people, planet, profits; all three going together. Then you had the birth of what we're calling environment social governance; ESG. So that kind of takes us to where I started where actually ESG wasn't yet a term in terms of where we started. But we started thinking about how these extra financial matters could affect long term value. I guess this is where you had the initial bifurcation between what we might call value and values. So you had a lot of people who were still thinking about it from an ethical lens, but you started to think about a lot of people who thought, "Well, actually there might be a lot of circumstances where if you do good by your customers, if you do good by your employers or employees, if you don't have environmental spillages, if you had good relationships for your regulators you would create long term value."

So a lot of people today can talk about stakeholder capitalism or enlighten shareholder value. You don't even have to produce the ESG terms. You just go, "Well, I'm looking about where long term value is." By serving my customers and by not having a good relationship with regulators you're going to get a lot of value. So a lot of the debate today now is around that. What is material to long term value creation? What might be value and what might be values? I think there's a lot of debate around that. I think I did want to pick up on two or three other things which have changed and this is in the nature of fund management itself. So again, if you go back 50 years ago, you did not have what we would call passive index funds, or rules based tilted funds, or quantitative funds. So that has changed the nature of stewardship voting and what we would call active ownership; so how to use your vote. But this idea of stewardship or active ownership actually goes back hundreds of years.

Link to podcast and transcipt here. Obv, take note of Jamie Dimon and not me in particular.

On arts, I saw a docu-drama - verbatim style on Grenfell. Dictating to the Estate. Guardian overview here.

I have not fully penned my thoughts here. I will say there is a lacuna re: ideas on the ultimate root cause here - what do we do about social housing and investing in it - and something about how the sub-contracting process, sub-contracts “risk” in a tick box fashion ultimately to those least able to assess and bear it (which is a little like Carillion). Acting and directing were good.

I also saw the biopic documentary on Stewart Brand. We Are As Gods. Several thoughts still swim in my head. First, the cost of drugs (and fame, pressure?) on his first marriage. Her last lines in the film “I am still cold” haunt me. Second, where does techno-optimism end and flying to close to the sun begin? I don’t know. Brand wants to bring back - de-extinct - the woolly mammoth. This might be both a possible positive climate idea, and be inspiring in the same way the (first) whole pictures of the Earth are/were. Or, it might be at best a waste of money, or at worst have negative unintended consequences. The film made me think I am not clever enough to know. Third, he has lived long enough for redemption/some dreams come true. A seemingly very happy life partnership, and seeing the American Chestnut trees become de-extinct.

Links:

London Climate week:

David Cutler: https://jamanetwork.com/journals/jama-health-forum/fullarticle/2792505 and https://www.boston.com/news/coronavirus/2022/05/17/harvard-economist-on-the-costs-of-long-covid-we-should-worry-about-it/